What Is an Automated Market Maker (AMM)?

An Automated Market Maker (AMM) is a decentralized exchange mechanism that prices swaps automatically. In a traditional exchange, buyers and sellers post bids and asks to an order book. A matching engine executes trades when prices line up. In an AMM, there is no need for that direct counterparty. The counterparty is the liquidity pool itself.

A liquidity pool is a smart contract that holds two or more assets. For example, an ETH/USDC pool holds ETH on one side and USDC on the other. Liquidity providers deposit assets into the pool and, in return, may receive a share of trading fees. Traders use the pool to swap one asset for another.

swap price impact between token A and token B.jpg">

swap price impact between token A and token B.jpg">

AMMs are most closely associated with decentralized exchanges, or DEXs. If you are new to the category, WEEX's page on Decentralized Exchange (DEX) is a useful companion concept because it explains the broader trading venue that AMMs often power.

How an Automated Market Maker Works

Most AMMs have three moving parts:

A liquidity pool that stores reserves of tokens.

A pricing formula that adjusts the exchange rate as pool balances change.

Liquidity providers who supply assets and may earn fees from swaps.

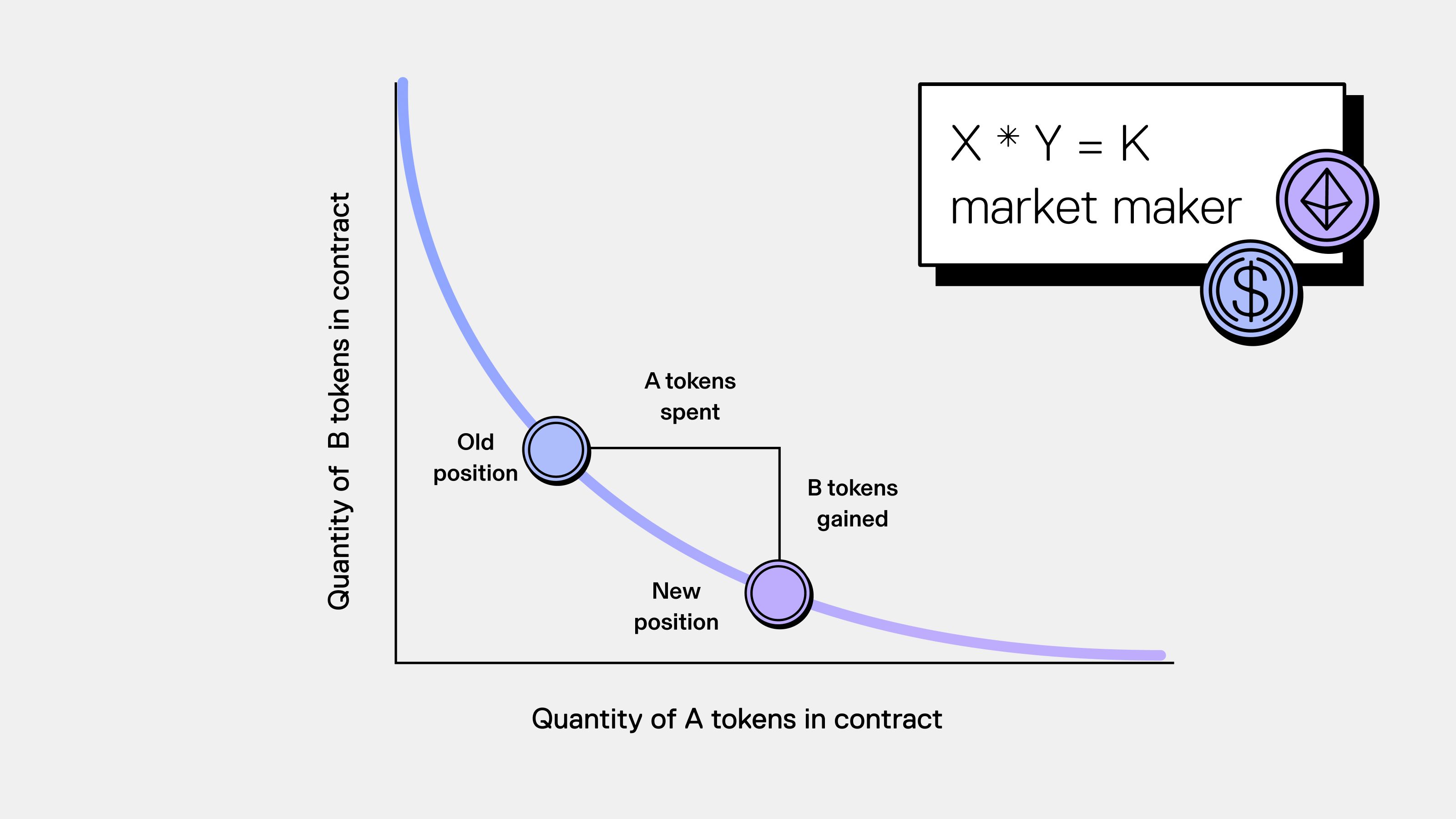

The classic formula is the constant product model:

x * y = k

In this formula, x is the amount of one token in the pool, y is the amount of the other token, and k is the constant product that the pool tries to preserve. When a trader buys token X from the pool, the pool's supply of X decreases and its supply of Y increases. Because the pool must preserve the relationship between the two reserves, the price of X rises as it becomes scarcer inside the pool.

Here is a simplified example. Suppose a pool holds 100 ETH and 300,000 USDC. The implied pool price is roughly 3,000 USDC per ETH before fees and price movement. If a trader buys a large amount of ETH, the ETH side of the pool shrinks. The AMM must quote a higher average price for each additional unit because the pool is being pushed away from balance. That difference between the expected price and the executed average price is price impact.

In practice, arbitrage traders help keep AMM prices close to broader market prices. If the AMM price drifts too far from centralized exchange prices or other DEX pools, arbitrageurs can trade against the pool until the spread narrows. This is useful for price alignment, but it does not remove execution risk for ordinary users.

AMM vs Order Book: The Key Difference

The main difference is where liquidity comes from. In an order-book exchange, liquidity comes from posted buy and sell orders. In an AMM, liquidity comes from token reserves inside smart contracts.

| Feature | Automated Market Maker (AMM) | Order-book exchange |

|---|---|---|

| Liquidity source | Liquidity pools funded by LPs | Bids and asks from traders and market makers |

| Trade counterparty | Smart contract pool | Another order or market maker |

| Pricing | Formula-based, driven by pool ratios | Market-driven, driven by posted orders |

| Common use | DEX swaps and DeFi apps | Centralized spot, futures, and advanced trading |

| Main execution risk | Price impact, slippage, thin pools | Spread, order-book depth, failed fills |

Neither model is automatically better. AMMs are powerful for permissionless on-chain swaps, especially when a token does not yet have deep centralized exchange liquidity. Order books are often more familiar for active traders who need limit orders, visible depth, and tighter execution on liquid markets. Readers who want to compare the order-book side can explore WEEX Spot after understanding how AMM execution differs.

Why AMMs Matter in DeFi

AMMs matter because they turned liquidity into open infrastructure. Before AMMs, decentralized exchanges struggled because thin order books made trading slow and inefficient. AMMs changed the problem by letting anyone create a pool and letting traders interact directly with that pool.

That matters for several reasons:

New tokens can become tradable without waiting for a centralized listing.

Liquidity providers can participate in market making without running a professional trading desk.

DeFi apps can compose with AMM pools for swaps, routing, collateral management, and yield strategies.

Markets can stay available 24/7 as long as the underlying blockchain and smart contracts operate.

This is why AMMs sit at the center of the wider Decentralized Finance (DeFi) stack. Lending markets, yield vaults, wallets, and portfolio tools often rely on AMM liquidity directly or indirectly.

Benefits of an Automated Market Maker

The biggest benefit of an Automated Market Maker (AMM) is continuous access. A trader does not need to wait for a matching seller. If the pool has enough liquidity, the trade can execute against the pool.

AMMs also lower the barrier to liquidity provision. In traditional markets, market making is usually a specialized business with infrastructure, inventory management, and risk systems. In DeFi, a liquidity provider can deposit token pairs into a pool and earn a portion of fees, though that does not mean the strategy is simple or low risk.

Another benefit is transparency. Pool reserves, fee tiers, token contracts, and many swap paths are visible on-chain. This does not make every pool safe, but it gives users more raw information than they would have in a closed system.

The final benefit is composability. AMM pools can plug into other smart contracts. Wallets, aggregators, lending protocols, and portfolio dashboards can route through them. That is one reason AMMs became a base layer for DeFi rather than just a trading feature.

Risks: Slippage, Impermanent Loss, and Smart Contract Exposure

The most common trader-side risk is slippage. Slippage is the difference between the price a user expects and the price they actually receive when the transaction executes. In AMMs, slippage can happen because the trade itself moves the pool price, or because other transactions hit the pool before yours confirms.

Price impact is related but not identical. Price impact comes from your trade size relative to the pool's depth. If you trade $1,000 against a deep ETH/USDC pool, price impact may be small. If you trade the same amount against a shallow new-token pool, the average execution price can move sharply.

For liquidity providers, impermanent loss is the risk that providing assets to a pool leaves them with a lower value than simply holding the same assets outside the pool. The word "impermanent" can be misleading. If the provider withdraws when token prices have diverged, the loss becomes realized. Trading fees may offset it, but they may not.

WEEX's Liquidity Mining entry is relevant here because many users first encounter AMM pools through reward campaigns. The practical rule is simple: do not evaluate liquidity provision only by headline rewards. Check token volatility, pool depth, fee volume, lockup rules, smart contract risk, and whether one token in the pair could collapse faster than fees can compensate.

Smart contract risk also matters. AMMs run on code. Bugs, admin-key issues, oracle manipulation, malicious tokens, and bridge exposure can all turn a normal-looking pool into a loss event. This is why experienced DeFi users check contract addresses, audits, permissions, and pool history before approving tokens or supplying liquidity.

Types of AMMs

Not every Automated Market Maker (AMM) uses the same design. The constant product model is the best-known version, but newer models try to solve specific weaknesses.

Constant product AMMs use x * y = k. They are simple, durable, and good for general token pairs, but large trades can face high price impact when liquidity is thin.

Stable swap AMMs are designed for assets that should trade near the same value, such as stablecoin pairs or wrapped versions of the same asset. They concentrate liquidity around the expected price range, which can reduce slippage for similar assets.

Weighted AMMs allow more flexible pool weights, such as 80/20 instead of 50/50. This can give liquidity providers different asset exposure, though it changes the pool's risk and slippage profile.

Concentrated liquidity AMMs let LPs provide liquidity inside chosen price ranges. This can make capital more efficient, but it also requires more active management. If price moves outside the selected range, the position may stop earning fees and become heavily exposed to one asset.

Examples of AMM protocols include Uniswap for general token swaps, Curve for stable swap pools, Balancer for weighted pools, Bancor for early automated liquidity models, and PancakeSwap for BNB Chain trading. Some pools also support wrapped Bitcoin assets, which lets Bitcoin-linked liquidity move through DeFi without native Bitcoin leaving its own network. Those examples show why AMM crypto markets are not one uniform category: the formula, asset pair, chain, and liquidity depth all change the user experience.

The more important point is that AMM design is never just a technical detail. It changes who takes risk, how much capital is needed, and what kind of trader receives good execution.

How to Prevent Bad AMM Execution Before You Trade

Before using an AMM, look beyond the quoted output amount. A good pre-trade check should include:

Pool depth: deeper liquidity usually means lower price impact.

Slippage tolerance: too tight can fail the trade; too loose can expose you to poor execution.

Token contract: verify that the asset is the real token, not a copycat.

Route: aggregators may split trades across pools, but the route still matters.

Fees and gas: a small swap can become inefficient if network costs are high.

Pool history: new pools can be thin, volatile, or manipulated.

Approval risk: avoid unlimited approvals to unknown contracts when possible.

For liquidity providers, add another layer of checks: expected trading volume, fee tier, impermanent loss risk, token volatility, unlock mechanics, and whether rewards are paid in a token with real liquidity. The users who get hurt most often are not always the ones who take the biggest risks; they are the ones who mistake a pool's displayed APY for a full risk analysis.

To defend against common AMM mistakes, treat every pool quote as conditional. Check the route, review the minimum output, verify the asset contract, and be careful with thin Bitcoin wrapper pools or newly launched token pairs where one side can drain quickly.

The Bottom Line

An Automated Market Maker (AMM) replaces the traditional order book with liquidity pools and formula-based pricing. It is one of DeFi's most important inventions because it makes token swaps open, programmable, and available without a centralized matching engine.

But the same design that makes AMMs accessible also creates specific risks. Traders need to understand price impact and slippage before swapping. Liquidity providers need to understand impermanent loss, smart contract exposure, and the difference between earned fees and realized profit.

Use AMMs when their strengths fit the job: on-chain swaps, long-tail tokens, DeFi routing, and permissionless liquidity. Use order-book markets when you need visible depth, limit-order control, or centralized execution tools. To keep building the vocabulary, continue with WEEX Crypto Wiki's guides to DeFi, DEXs, and liquidity mining, then compare those concepts with live crypto markets on WEEX.

FAQ

What is an AMM in crypto?

An AMM in crypto is an Automated Market Maker, a smart contract mechanism that lets users swap tokens through liquidity pools instead of matching buy and sell orders through a traditional order book.

How does an Automated Market Maker set prices?

An AMM sets prices through a formula based on pool reserves. In the common x * y = k model, the price changes as one token becomes more or less available inside the pool.

Is an AMM the same as a DEX?

No. A DEX is the decentralized exchange interface or protocol category. An AMM is one mechanism a DEX can use to provide liquidity and execute swaps.

Can liquidity providers lose money in an AMM?

Yes. Liquidity providers can lose money through impermanent loss, token price collapses, smart contract exploits, poor fee volume, or withdrawing at an unfavorable time.

Why do AMM swaps have slippage?

AMM swaps have slippage because pool prices can change during execution. The trade itself may move the pool ratio, and other transactions may execute before yours confirms.

Are AMMs better than order books?

AMMs are better for permissionless on-chain swaps and long-tail DeFi liquidity. Order books are often better for advanced trading controls, visible market depth, and liquid centralized markets.

You may also like

How to Buy Cryptocurrency on WEEX Exchange 2026: Full Guide

Prediction Market Apps 2026: How Prediction Markets Work? Are They Safe and Legal?

Is Polymarket Legal in India in 2026? Key Legal Updates on Prediction Markets

14 Best Prediction Market Apps in 2026: The Ultimate Guide to Crypto-Native and Regulated Platforms

Can Politicians Rig Election Prediction Markets? The Dark Side of Election Prediction Markets

2026 US Election Odds: Who Leads Right Now on Polymarket and Kalshi?

What Is a Crypto Prediction Market? Key Opportunities in the Prediction Market Sector

Plot twist in the AI race—the next big flex is actually physical infra?

How to Profit on Prediction Market: A Beginner's Guide to Prediction Market

Decentralized Prediction Market: A Beginner's Guide for WEEX Users

Kalshi Prediction Market Explained: How It Works and Who Can Use It

What Is WXT Used For? A Beginner's Guide to WEEX Token Utility

Top Prediction Market Websites in 2026: Which Platform Is Best for You?

How to Start Spot Trading on WEEX: No Leverage, No Liquidation Risk

What Is a Prediction Market Platform? How It Works and Key Risks

Can You Make Money on Prediction Markets? Risks and Strategies

Is a Prediction Market Just Gambling? How It Works and Key Risks